Christian Ruggiero, Maria Romana Allegri, Stefania Parisi, Mauro Bomba, Emma Garzonio, Camillo Cantarano, Marco Galluccio, Laura Valentini

Italy is a southern European country with a population of 58,983,122 (28,747,417 male and 30,235,705 female). Nearly the entire Italian population has access to a wide variety of media, and over 80% also accesses information content daily (AgCom, 2018a).

More than three-quarters of the Italians use different media for information purposes. For years, television has been the most used news media – in 2018 more than 90% of the Italian population used television to access information (AgCom, 2018a) – while after the Covid-19 pandemic it has lost its primacy to web sources and social networks (Reuters, 2022). Despite Italy being ranked at the bottom of the Desi index on connectivity in terms of access to the internet, in 2021 83.7% of the population used the Internet and 67.9% used social networks.

Over the past decade, newspapers have been experiencing a structural crisis reflected in decreasing sales. Both the sectoral economic crisis and the difficulties in achieving full digitalisation have caused media companies to lose more than €2 billion over the last ten years (AgCom, 2022). These economic issues are among the causes of the problematic distribution of newspapers in some areas of Italy, like remote communities and islands.

Within the media landscape, large media groups often belong to prominent Italian entrepreneur families. The publishing group Gedi, linked to the Agnelli family, and Fininvest, the media company built by Silvio Berlusconi and mainly administered today by his family members, are the two clearest examples of this trend.

The 18 analysed outlets (8 TV channels, 6 print newspapers, 4 digital newspapers – of which 2 web-only) have been selected against criteria of market share, impact revenues, audience share, and unique political and institutional affiliations, the latter being considered of particular relevance to offer a broad and detailed representation of the Italian media sector.

Among the TV channels, six outlets belong to the two biggest TV operators in Italy: the public broadcasting service Rai (respectively Rai 1, 2, 3) and the private corporation Mediaset (Italia 1, Rete 4, Canale5). They alone collect most of the share and revenues nationwide. Below them stands LA7, owned by Cairo Communication: despite being positioned at a considerable distance from the Rai/Mediaset duopoly in terms of share, it is considered the “third pole of Italian broadcasting”. The last TV outlet considered is SkyTg24, owned by Comcast group: it’s the most relevant all-news channel in Italy, owned by a non-Italian media operator.

Tab.1 – Impact of revenues (%)

| Group | % |

|---|---|

| ComCast/Sky | 35.6 |

| RAI | 29.0 |

| Fininvest/Mediaset | 19.9 |

| Others (national) | 6.8 |

| Digital platforms | 5.1 |

| Local broadcasters | 3.6 |

Tab. 2 – Television: national market share in terms of audience (%)

| Broadcaster | Average daily share on an annual base |

|---|---|

| Rai | 35.7 |

| Fininvest/Mediaset | 31.6 |

| Others | 12.3 |

| Discovery | 7.4 |

| Comcast/Sky Italy | 7.2 |

| Cairo communication | 4.2 |

| Viacom | 1.6 |

Concerning the press sector, the selected outlets reflect, on the one hand, the existence of two large media ownership groups (Repubblica is owned by Gedi, Il Corriere Della Sera belongs to the Cairo/RCS group) and, on the other, the existence of specific affiliations of different nature and particular interest within the country’s media landscape.

The most relevant examples are Il Giornale, owned by the Berlusconi family and close to his party and the centre-right coalition’s political claims; Il Sole 24Ore, the most prominent economic newspaper owned by Confindustria, the entrepreneurs’ union; and Avvenire, a Catholic nationally distributed newspaper that is owned through a religious foundation by the Italian Episcopal Conference (CEI), the permanent council of Italian bishops, an ecclesiastic governing body directly appointed by the Pope and ruled by the Vatican State.

Tab. 3 - Press market share

| Groups | % |

|---|---|

| Gedi (La Repubblica*, La Stampa) | 25.4 |

| Cairo/RCS (Il Corriere della Sera*; La Gazzetta dello sport) | 21.5 |

| Monrif (QN, Quotidiano Nazionale) | 8.3 |

| Caltagirone Editore (Il Messaggero, Il Mattino, Leggo) | 7.0 |

| Gruppo 24 Ore (Il Sole 24 Ore*) | 5.4 |

| Gruppo Amodei (Tuttosport and Corriere dello sport) | 3.2 |

| Others* | 29.2 |

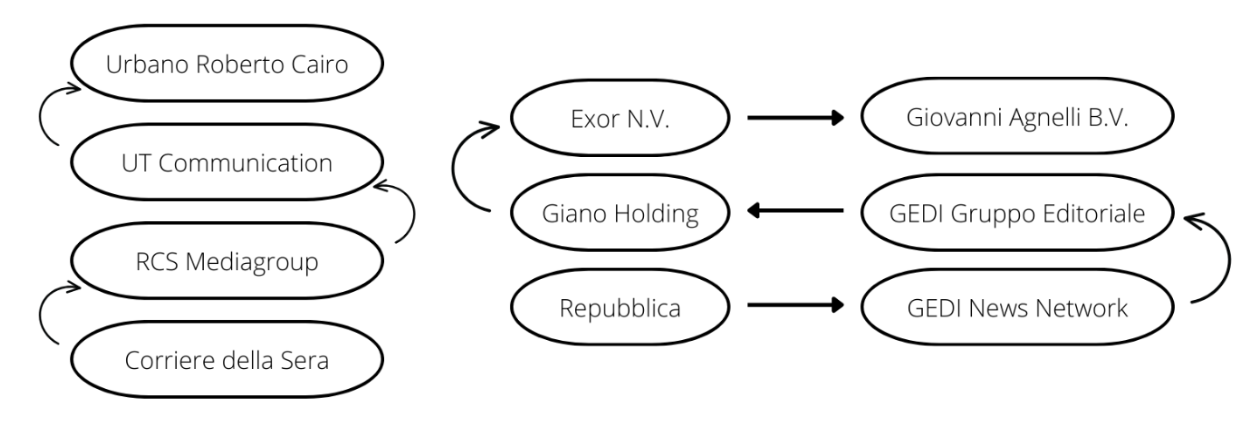

The Italian media ownership system is quite complex. A consolidated tendency that emerged from the analysis of the financial reports of the selected media companies is the “Chinese box” (Treccani, 2012) ownership structure, in which a holding controls multiple companies – and ultimately, their outlets – through a chain of sub-holding. The final owner is thus allowed to control the outlet through his/her society atop the ownership pyramid, rather than owning the majority of its shares – considering that the majority shareholder is the one who possesses more than 50% of the share capital. Such a system makes it harder to recognise which natural or legal person owns the outlet.

To provide an example of such a structure, the diagrams below illustrate the ownership chain of two selected print media outlets, Repubblica and Il Corriere Della Sera.

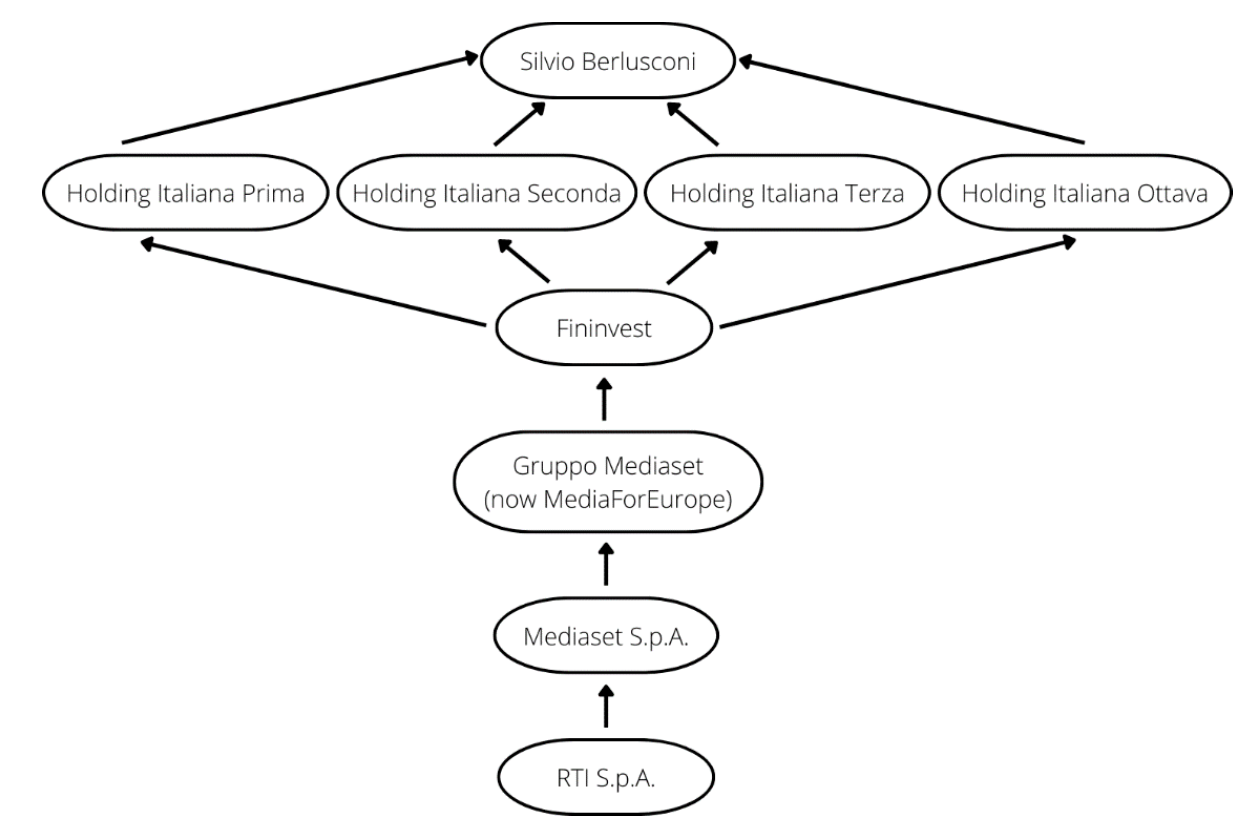

The same situation applies to Mediaset outlets (Rete 4, Canale 5, Italia 1). Silvio Berlusconi – entrepreneur, former Italian prime minister and well-known for his controversial career and private life – is formally a member of the society’s financial board. However, the ownership chain unveils him as the final hidden owner because he owns, through four different holdings, 61% of Fininvest’s shares, the latter owning 51% of Mediaset group as shown in the diagram below:

Moreover, Fininvest is a family-owned company, which means that the remaining part of its shares belongs to other members of the Berlusconi family. Berlusconi’s media empire also includes Il Giornale, whose main shareholder is Società Europea di Edizioni, owned by Paolo Berlusconi, Silvio’s brother. This media outlet constitutes a vivid example of contested ownership: without being its real owner, Silvio Berlusconi has the actual power to influence the editorial line and the choice of editors-in-chief of the newspaper.

Exor NV group and the Agnelli family (one of the oldest and most powerful families of Italian entrepreneurs) represent another sample of the complexity of ownership chains in Italy. Exor indeed owns – in addition to the already mentioned Repubblica – other Italian newspapers and media outlets, such as La Stampa and Il Secolo XIX, through the same Gedi group. Some radio outlets (such as Radio Deejay and Radio Capital) and magazines (National Geographic, Limes) also belong to different editorial companies that Gedi ultimately owns.

Many of the analysed ownership groups show relevant connections with foreign ownership: Exor owns The Economist Group, editor of the British newspaper The Economist; Mediaset owns Mediaset España, and it also has relevant shares of the German ProSieben.Sat1 TV company and the Tunisian TV channel Nessma; through its parent company Unidad Editorial, RCS publishes El Mundo and Marca, two prominent Spanish newspapers.

Information on the composition of the editorial staff of the examined outlets is often missing from the financial reports. Indeed, such data is usually presented as aggregated, and not split off into the specific media outlet or specific functions within the same outlet (e.g., the data concerning the number of employed journalists is available for Rai S.p.a. but not for the single outlets Rai1, Rai2, and Rai3).

Further data that are often not published in the financial reports concern types of public subsidies. The reports do not usually declare public financing figures, although citizens may benefit from open and transparent data published from government sources (like the Information and Publishing Department). While we can assess a certain degree of transparency concerning direct public financing, the same can’t be said for indirect funding sources. For example, companies must declare income sources generated from institutional advertising (publishing funds for advertising) to the Italian National Regulatory Authority (AgCom), but – as the Legal framework section will show in detail – the NRA does not make these data available and public.

Another reason why most indirect public funding sources are harder to track is that, sometimes, the aid recipients are not the outlets themselves, but rather the non-media enterprises owning them. One exception is tax credits for paper supply: despite the lack of explicit references within the financial reports, institutional sources allowed for the tracking of the beneficial companies (Dipartimento per l’Informazione e l’Editoria della Presidenza del Consiglio dei Ministri, 2022).

Despite the decreasing trend shown by public funding in the last decade, with its serious consequences for the publishing sector, the 2021 report of the Department for Information and Publishing states that in Italy the figures for public subsidies rose from €175.6 million to €386.6 million, an increase of 120%. Such an increase follows a general trend in Europe of public investment in support of print media, especially during the Covid-19 pandemic. In Italy, in 2021, direct public subsidies accounted for €88 million (against the €180 million in 2011), indirect funding stood at €64.5 million and tax reliefs accounted for €233 million (Paganessi, 2022). Tax reliefs, in general, are not recorded in financial reports, but they still constitute an extremely relevant source of financing.

The decreasing trend of direct financing started with Law 2016/198, which downsized the number of newspapers eligible for public funding. One of the consequences was a certain instability in terms of ownership: in 2016, Cairo Communication bought RCS from Exor, which acquired Gedi Group four years later. The difficult financial situation forced Exor itself to sell the investigative tabloid L’Espresso in 2022, and many newspapers had to cease their activity, such as the long-standing L’Unità, in 2017. This decline can be understood in terms of newspapers not being considered an asset. The number of readers in Italy is indeed showing a negative trend since 2005 (Ruffino, 2021; Vespignani & Farneti, 2017). Print media now represent just the fourth most used source of information, used by only 18% of the Italian population (Cornia, 2021). In 2013, the share was 60%.

The main risks to transparency in the country are represented by complex ownership chains, lack of data within the financial reports leading to difficult traceability of information, and an intricate funding system that is often non-transparent for citizens.

The first element worth mentioning, which refers to issues widely reported in academic literature, is the proximity of publishers and owners to political parties and interest groups.

A relevant kind of affiliation is the political one. The case we were able to track down regards the Mediaset group: Silvio Berlusconi is the group’s hidden owner and at the same time he’s still active in his political career as the lead candidate of his party, Forza Italia. Other examples of affiliation concern Avvenire, a newspaper owned by a Catholic governing body (CEI), and Il Sole 24 Ore, the leading economic newspaper in Italy, owned by Confindustria, the Italian entrepreneurs’ guild.

The second dimension of interest concerns those media owners who have relevant economic interests in sectors outside publishing and show links to industrial companies, financial groups or political parties. Tracking different kinds of affiliation between the analysed outlets and their owner’s collateral societies, some relevant examples of the existence of such kinds of connections emerge. We have media owners with a large and diverse pool of non-media-related financial assets: Exor (owner of Fiat Chrysler Automobiles, Stellantis, Juventus football club and shareholder of mechanical industries such as Iveco, oil and gas companies such as Welltec, fashion companies such as Louboutin and Shang Xia, among others) and Fininvest (owning Mediolanum Bank and Monza football team). Only one of the cases considered, Cairo Communication, comes closest to the type of “pure publisher”, with media-centred interests: its president, Urbano Cairo, holds the presidency of RCS group and Torino football club.

According to the main reports on news consumption in Italy (Censis, 2022; AgCom, 2018a), television is the most widespread news media source.

Print media are particularly threatened by the increase in digital media consumption: the daily newspapers sold in 2020 show around half of the figures registered in 2013 (Santoro, 2021), confirming the decreasing trend already mentioned in the previous paragraphs.

As the AgCom Report on news consumption (2018a) underlines, 54.5% of the Italian population access online news mainly by algorithmic sources (social networks and search engines). Publishing sources (websites and applications by traditional publishers and native digital news services) are less used; 19.4% of Italians claim that an algorithmic source is their main channel of news consumption.

Alphabet and Meta show a hegemonic position within the digital landscape when it comes to online news consumption. Censis data (2019) shows that in Italy, the main digital intermediaries are Facebook (31.4%), Google (20%) and YouTube (11.9%).

The Desi Index (2020) has been created to measure inequality concerning Internet access. Italy is positioned below the EU average (20/27) and lost further four positions in this ranking in 2021 (24/27).

Newspaper distribution presents many criticalities, too. Many sources report difficulties in delivering daily national newspapers to remote areas, particularly to the main islands of Sicily and Sardinia. Such criticism in distribution is due to the ongoing crisis in the Italian publishing sector (Mastrandrea, Melis & Di Natale, 2022).

The broadcasting infrastructure of radio and TV frequencies is, de-facto, a duopoly, composed of Raiway (shared at 65% by Rai S.p.A) and EI Towers (owned at 60% by Fondi Italiani per le Infrastrutture (F2I) and 40% by Mediaset).

The Prime Minister Decree issued on February 17th, 2022, allowed Rai to sell its Raiway shares up to 30%. Contextually, many news sources reported the interest of EI Towers in purchasing these shares; others even hypothesised a merger (Fontanarosa, 2022). A previous attempt in this sense was realised in 2015, but it was eventually blocked by the antitrust authority (AGCM, 2015) which feared this scenario would have compromised the conditions of competition, since a fusion could create a monopoly and an unfavourable situation for smaller players, potentially excluded from the access to radio and TV infrastructures.

In Italy, most of the discipline on audio-visual media is contained in Law 2021/208, that is the Consolidated Text of Audio-visual Media Services (original name, Testo Unico Dei Servizi Media Audiovisivi, Tusma), which implements the EU Directive 2018/1808. Moreover, other general laws regulate issues of ownership transparency and market stability, respectively remitted to Art. 2435 of the Civil Code, Law 2015/139, and Law 1990/287.

The latter, broadening article 43 of the Italian Constitution, institutes the National Regulation Authority for Market Competitiveness (Autorità Garante per la Concorrenza nei Mercati, AGCM).

Concerning the media sector, Law 1996/650 compels printed media outlets to publish their parent company’s financial report on their pages, before August 31st of any year. This conforms with the requirements of transparency in the media sector stated by article 21 of the Italian Constitution.

The Italian NRA for the media sector is the Authority for Communication Guarantees (Autorità per le Garanzie nelle Comunicazioni, AgCom). With the deliberation n° 2008/666, the NRA instituted the Communication Operators Register (Registro degli Operatori di Comunicazione, ROC), to which every operator in the media sector is compelled to apply. This register also includes the financial reports and information regarding institutional advertising profits.

Article 5 of the EU Directive 2018/1808 has been fully transposed by Art. 29, 3 of Tusma, and even anticipated by article 2435 of the Civil Code, dating back to 1942. This provision obliges every Italian company, and every foreign enterprise with an Italian branch as well, to send their financial report, list of associates, and shareholders, to the local Register of Companies.

Looking specifically at the media sector, the Constitutional Law 1948/47 anticipated not only the provisions stated by article 5 of the EU Directive 2018/1808 but also part of the content of article 4.4 of the Recommendation CM/Rec(2018)1 of the Council of Europe. In particular:

It’s worth remarking that the implementation of the EU Directive 2018/1808 in the Italian law happened with a severe delay, compared to the European Commission’s expectations. Such setback led to the opening of an infringement procedure against Italy in November 2020 (European Commission, 2020; 2021). The Directive has been finally transposed in November 2021, just before the deadline imposed by the European Commission to the Italian government.

Although Law 1996/650 obliges the owners of printed outlets to publish their financial reports on their newspapers, it is still hard for ordinary citizens to retrieve these data. In many cases, such information is accessible only by paying a fee to the National Register of Companies. For instance, this is what happened for this data collection: the Italian research team had to buy nine reports from the Register, paying €2.50 each

Moreover, despite AgCom requires all media enterprises in Italy to sign up to the ROC, for the most part the latter is off-limits to the public. The only publicly available data are the ones stated by article 5 of the EU Directive 2018/1808 (i.e., the media service provider’s name, geographical address, and contact details). This leaves out most of the data which, according to the Recommendation CM/Rec(2018)1 of the Council of Europe, would foster correct information about the real state of media pluralism in the country.

Concerning digital intermediaries’ regulations, the intervention of the Italian lawmaker is limited to the literal application of EU Directives – as in Law 2003/73 (enforcing the EU Directive 2000/31/EC on e-commerce and juridical aspects of IT services in the Internal Market) – and emission of non-binding guidelines, as in the case of the regulation of online par condicio during election campaigns issued by AgCom in 2018 (AgCom, 2018b). For questions related to content curation and sponsored advertising labelling, the Italian lawmaker usually relies on societal best practices, which detail their features in the Terms and Conditions of their platforms. The first step toward more conspicuous intervention by the authority against digital intermediaries comes from two AgCom Council Resolutions, No. 275/22/CONS (AgCom, 2022b) and No. 288/22/CONS (AgCom, 2022c), challenging the violation of the ban on advertising winnings on the online casino not only to the company producing the videos themselves, but also to YouTube, and thus to Google Ireland Limited (Vita, 2022).

AGCM (Autorità Garante per la Concorrenza nei Mercati / Regulation Authority for Market Competitiveness). (2015, May 11). Istruttoria dell’Antitrust sull’Opas EI Towers-Rai Way / Antitrust investigation into the EI Towers-Rai Way Opas. Retrieved from https://www.agcm.it/media/comunicati-stampa/2015/3/alias-7536

AgCom (Autorità per le Garanzie nelle Comunicazioni / Authority for Communications Guarantees). (2018a, February 1). Linee guida per la parità di accesso alle piattaforme online durante la campagna elettorale per le elezioni politiche 2018 / Guidelines for equal access to online platforms during the 2018 general election campaign. Retrieved from https://www.agcom.it/documents/10179/9478149/Documento+generico+01-02-2018/45429524-3f31-4195-bf46-4f2863af0ff6?version=1.0

AgCom (Autorità per le Garanzie nelle Comunicazioni / Authority for Communications Guarantees). (2018b, February 1). Rapporto sul consumo di informazione / Report on the news consumption. Retrieved from https://www.agcom.it/documents/10179/9629936/Allegato+19-2-2018/22aa8cab-a150-449e-ad57-94233644cbe5?version=1.0

AgCom (Autorità per le Garanzie nelle Comunicazioni / Authority for Communications Guarantees). (2020, July 6). Relazione annuale 2020 / annual report, year 2020. Retrieved from https://www.agcom.it/documents/10179/19267334/Documento+generico+06-07-2020/d0962b60-452c-4477-9677-0c7f447a425e?version=1.0

AgCom (Autorità per le Garanzie nelle Comunicazioni / Authority for Communications Guarantees). (2022a, April 22). Osservatorio sulle comunicazioni n° 1/2022 / communication markets monitoring system no. 1/2022. Retrieved from https://www.agcom.it/documents/10179/26662003/Documento+generico+22-04-2022/8a827676-223a-4e23-ae3c-023f19176288?version=1.2

AgCom (Autorità per le Garanzie nelle Comunicazioni / Authority for Communications Guarantees). (2022b, July 19). Delibera n. 275/22/CONS. Ordinanza-ingiunzione nei confronti della società Google Ireland Limited per la violazione della disposizione normativa contenuta nell’art. 9, comma 1, del decreto-legge 12 luglio 2018, n. 87 convertito con legge 9 agosto 2018, n. 96 (cd. decreto dignità) (cont. n. 3/22/dsdi – proc. n. 5/fdg) / Resolution No. 275/22/CONS. Order-injunction against the company google ireland. Retrieved from https://www.agcom.it/documents/10179/27283847/Delibera+275-22-CONS/be09989c-a5dd-4723-a5b5-a61cf29d0a95?version=1.0

AgCom (Autorità per le Garanzie nelle Comunicazioni / Authority for Communications Guarantees). (2022c, July 27). Delibera n. 288/22/CONS. Ordinanza-ingiunzione nei confronti della società top ads ltd per la violazione della disposizione normativa contenuta nell’art. 9 del decreto-legge 12 luglio 2018, n. 87 convertito con legge 9 agosto 2018, n. 96 (cd. decreto dignità) (contestazione n. 4/22/dsdi) / Resolution No. 288/22/CONS. Order-injunction against the company top ads ltd for violation of the regulatory. Retrieved from https://www.agcom.it/documents/10179/27283847/Delibera+288-22-CONS/45f1985b-9407-4da6-82ae-61c7088a9ce0?version=1.0

Auditel. (2020). Sintesi settimanali e mensili degli ascolti televisivi, anno 2020 / Monthly and wwekly report of TV ratings, year 2020. Retrieved from https://www.auditel.it/dati/

Censis. (2020). Sedicesimo Rapporto sulla Comunicazione / 16th Report on Communication. Milan: FrancoAngeli.

Censis. (2021). Diciassettesimo Rapporto sulla Comunicazione / 17th Report on Communication. Milan: FrancoAngeli.

Cornia, A. (2021, June 23). Italy – Digital News Report 2021. Retrieved from https://reutersinstitute.politics.ox.ac.uk/digital-news-report/2021/italy

Dipartimento per l’Informazione e l’Editoria della Presidenza del Consiglio dei Ministri / Department of Information and Publishing of the Presidency of Council of Ministers. (2022, April). Elenco dei soggetti ammessi al credito d’imposta per l’acquisto della carta – Anno 2021 – Allegato alla Delibera del 7 aprile 2022 / List of entities eligible for the paper purchase tax credit – Year 2021 – Annex to the April 7, 2022 Resolution. Retrieved from https://www.editoria.tv/wp-content/uploads/2022/04/Elenco-beneficiari-2021-anno-2020.pdf

Enciclopedia Treccani. (2012). Scatole cinesi in “Dizionario di Economia e Finanza”. Treccani, il portale del sapere. https://www.treccani.it/enciclopedia/scatole-cinesi_(Dizionario-di-Economia-e-Finanza)/

European Commission. (2020a). DESI by components – Connectivity, year 2020. Retrieved from https://digital-agenda-data.eu/charts/desi-components#chart=%7B”indicator”:”desi_conn”,”breakdown-group”:”desi_conn”,”unit-measure”:”pc_desi_conn”,”time-period”:”2020″%7D

European Commission. (2020b, November 23). Audiovisual Media: Commission opens infringement procedures against 23 Member States for failing to transpose the Directive on audiovisual content. Retrieved from https://ec.europa.eu/commission/presscorner/detail/en/ip_20_2165

European Commission. (2021). Stepping up legal action: Commission urges 19 Member States to implement EU digital and media laws. Retrieved from https://ec.europa.eu/commission/presscorner/detail/e%20n/ip_21_4612

Fontanarosa, A. (2022, March 8). Viale Mazzini al 30% in Rai Way. Il decreto del governo: “Avrà il controllo” (Viale Mazzini at 30 percent in Rai Way. Government decree: “It will have control”). La Repubblica. Retrieved from https://www.repubblica.it/economia/2022/03/08/news/viale_mazzini_al_30_in_rai_way_avra_il_controllo-340707488/

Mastandrea, A., Melis, M., & Di Natale, R. M. (2022, April 2). Dove i giornali sono un ricordo (Where newspapers are a memory). L’Essenziale. Retrieved from https://www.internazionale.it/essenziale/notizie/angelo-mastrandrea/2022/04/12/distribuzione-giornali

Newman, N., Fletcher, R., Robertson, C. T., Eddy, K., & Nielsen, R. K. (2021). Reuters Institute Digital News Report 2022. Oxford: Reuters Institute for the Study of Journalism. Retrieved from https://reutersinstitute.politics.ox.ac.uk/sites/default/files/2021-06/Digital_News_Report_2021_FINAL.pdf

Paganessi, I. (2022, June 7). Il finanziamento pubblico ai giornali è raddoppiato durante la pandemia (Public funding for newspapers doubled during the pandemic). L’Indipendente. Retrieved from https://www.lindipendente.online/2022/01/02/il-finanziamento-pubblico-ai-giornali-e-raddoppiato-durante-la-pandemia/#:~:text=Nel%202021,%20inoltre,%20lo%20Stato,solo%20al%205%%20delle%20copie

Ruffino, L. (2021, November 6). I quotidiani in Italia sono sempre meno letti (Newspapers in Italy are getting less read). YouTrend. Retrieved from https://www.youtrend.it/2021/11/16/i-quotidiani-in-italia-sono-sempre-meno-letti/

Santoro, P. L. (2021, March 10). Il Trend di Vendite dei Quotidiani in Italia dal 2013 al 2020 (The Trend of Newspaper Sales in Italy from 2013 to 2020). DataMediaHub. https://www.datamediahub.it/2021/03/10/il-trend-di-vendite-dei-quotidiani-in-italia-dal-2013-al-2020/

Vespignani, F., & Farneti, E. (2017, December 28). Giornali italiani, le vendite stentano ma i lettori resistono (Italian newspapers, sales stall but readership endures). Il Fatto Quotidiano. https://www.ilfattoquotidiano.it/2017/12/28/giornali-italiani-le-vendite-stentano-ma-i-lettori-resistono-1/4023445/amp/

Vita, V. (2022, August 10). Google e You Tube nel mirino dell’Agcom (Google and YouTube under Agcom’s scope). Articolo21. https://www.articolo21.org/2022/08/google-e-you-tube-nel-mirino-dellagcom/

Country report published in September 2022